There's an old joke that goes something like this: teach a parrot to say ‘supply and demand' and you've created an economist. And, honestly, there is some truth to this common trope; after all, economics is not called the ‘dismal science' for no reason. However, even with all the criticisms, the economic laws of supply and demand provide an excellent model for explaining how numerous markets work, as well as what goes wrong when those markets fail. Supply and demand also shows why the costs of President Trump's steel tariffs could be steep for American consumers.

In case you missed it, President Trump announced in March 2018 that he would be imposing a 25% tariff (a nice round number) on steel imports coming into the US. The hope is that these tariffs would stimulate domestic steel production and lead to more jobs in the steel industry. However, because economists know trade wars are not easy to win, they have been squawking ‘supply and demand' ever since.

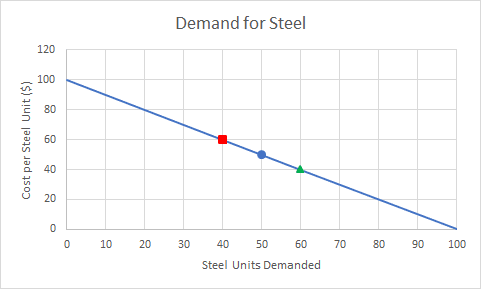

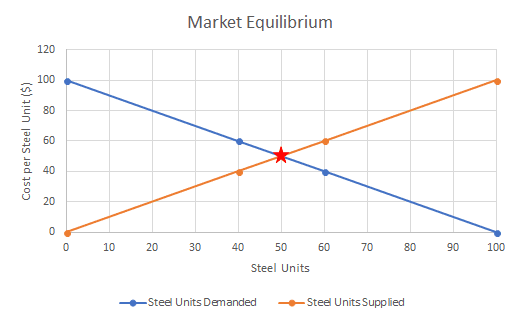

The primary idea behind demand is that, as prices for a product go up, demand for that product goes down. Likewise, as prices go down, demand goes up. Let's say, hypothetically, that a unit of steel costs $50 in the US, and at that price people in the market are willing to buy 50 units (blue dot on the demand graph). Now, let's say there's a yuge steel sale and prices drop to $40 (green triangle); people are now willing to buy 60 units. However, if prices were to be raised to $60 (sad!), people would only be willing to buy 40 units (red square).

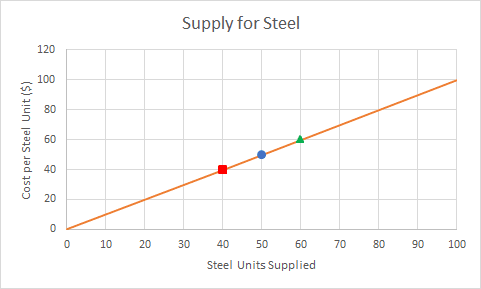

Supply works in much the same way, only in reverse. So, in our steel example, at $50, businesses will make 50 units of steel (blue dot on the supply graph). At $60, businesses will make 60 units (green triangle). Simple, right? Even the parrot is probably still with us.

The sweet price spot where the units supplied and demanded are equal is called the market equilibrium (red star on the market equilibrium graph). In our example, the market equilibrium is 50 units of steel at $50 each. At this point, there is no excess supply or shortages – it's the greatest steel market ever!

Like many commodities, though, steel isn't just an American product – it's traded on a global market, where countries differ in their steel producing capabilities. China produces about half the world's steel due to an extensive network of steel mills. This massive steel industry allows China to make a lot of steel very cheaply (in technical terms, China has a comparative advantage). This has the result of driving steel prices down, at which point many American businesses can no longer turn a profit. Unfair!

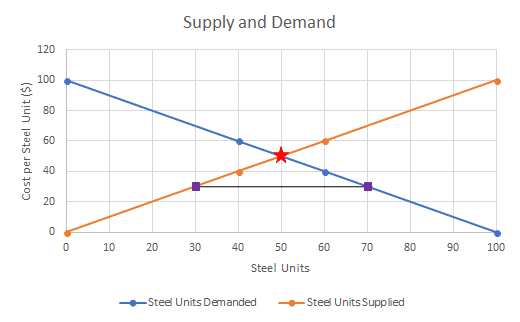

This also means the US market is no longer at equilibrium. Steel is sold at a low price, which increases demand to a point beyond what the US steel industry can provide. Let's say that China's steel supply pushes prices down to $30. At that price, demand for steel is 70 units, but US businesses can only produce 30 units; this means there's a deficit in the US supply of 40 units (line between the two purple squares on the supply and demand graph). To make up this deficit, industries that use steel import it from other countries.

Tariffs attempt to move domestic markets back to equilibrium by taxing imports, artificially raising a product's price. Since steel is more expensive with tariffs, US steel businesses can produce more of it. This leads to more jobs in the steel industry – winning big league!

While putting tariffs on imported steel may seem like the best deal ever for the US, it's not. Without tariffs, businesses that utilize steel in their products (e.g. construction, cars, shipping) will import it from other countries at a cheap price. This not only lowers the costs of those products (e.g. cheaper cars and homes), the resulting increased demand (e.g. more cars and homes) leads to the creation of jobs in those industries. However, by interfering with the supply and demand of steel, negative effects are felt in these other industries: their prices go up (which affects everyone), demand falls, and jobs are lost. It's been estimated that President Trump's steel tariffs will create 27,000 steel jobs, all the while costing 430,000 jobs in other industries.

While the stagnation of the US steel industry has led to many problems, propping it up with bad policy will only cause harm to the overall economy. If he really wants to make America great again, perhaps President Trump would be wise to listen to our feathered economist about supply and demand.

About the Author

A transplant from Virginia (Hoos!), Greg Evans is a grad student at UGA, finishing up a Master’s in Plant Biology and beginning a Master’s in Ag Business. He enjoys boxing, board games, and gardening. Greg currently serves as an Associate Editor for the Athens Science Observer, as well as the Athens Science Alliance Liaison. He can be reached at gevans@uga.edu and followed on Twitter @WeedyInvasive. More from Greg Evans. A transplant from Virginia (Hoos!), Greg Evans is a grad student at UGA, finishing up a Master’s in Plant Biology and beginning a Master’s in Ag Business. He enjoys boxing, board games, and gardening. Greg currently serves as an Associate Editor for the Athens Science Observer, as well as the Athens Science Alliance Liaison. He can be reached at gevans@uga.edu and followed on Twitter @WeedyInvasive. More from Greg Evans. |